|

IFRS 17 Insurance contracts - Part 3

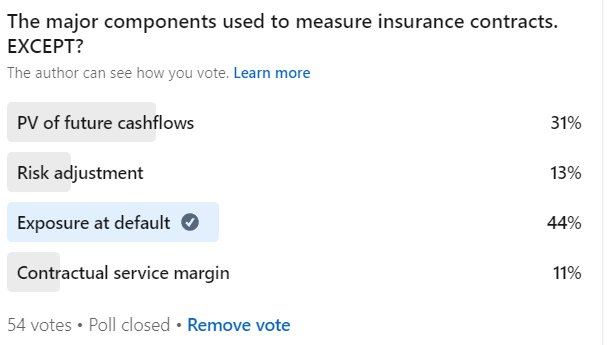

I raised a poll on IFRS is easy's LinkedIn page and here is the result.

|

| Note that the results here are not necessarily correct. Please continue reading for the correct answer. |

If you are familair with IFRS 9, you most likely still remember the components that we consider in testing for impairment on financial assets.

To jug your memory, they are Exposure at Default (EAD), Loss Given Default (LGD) and Probability of Default (PD). I will discuss these and the required computations in later posts after completing the IFRS 17 introduction series.

There are 3 major components in measuring insurance contracts:

1. Present value of future cash flows

2. Risk adjustment

3. Contractual service margin

Now let's talk briefly through them.

Present value of future cash flows

When an insurance company receives premiums from the policyholder, many times, the premiums are not one-off. They are often annual payments made by the policyholder over the insurance coverage period. And as you already know, the time value of money always kicks in when cash flows are over a period of time. This is the reason why we are talking about present value.

Simply, the present value of future cash flows is the financial risk of the insurance contract. It represents the discounted inflows (premiums) and outflows (expected claims to be paid to the policyholder, acquisition cost incurred in winning over the policyholder and other direct expenses).

Risk adjustment

This is the compensation to the insurer for bearing the non-financial risk of insuring the policyholder.

Contractual service margin

This is the unearned profit of the insurer that is amortised over the insurance coverage period.

There's a fourth guy in the wheel called the "Fulfillment cash flows". This is simply the addition of the present value of future cash flows and the risk adjustment.

Yes! You made it to the end.

I will be happy to receive any questions you may have about the topic discussed in this blog post.

Share in the comment section about the misconceptions you once had about IFRS 17.

Don’t forget to subscribe to our YouTube channel to get all new IFRS analyses. Also, click on the email subscription button on this page so as not to miss any of our blog updates.

Written by:

Adedamola Otun

For: IFRS IS EASY

No comments:

Post a Comment